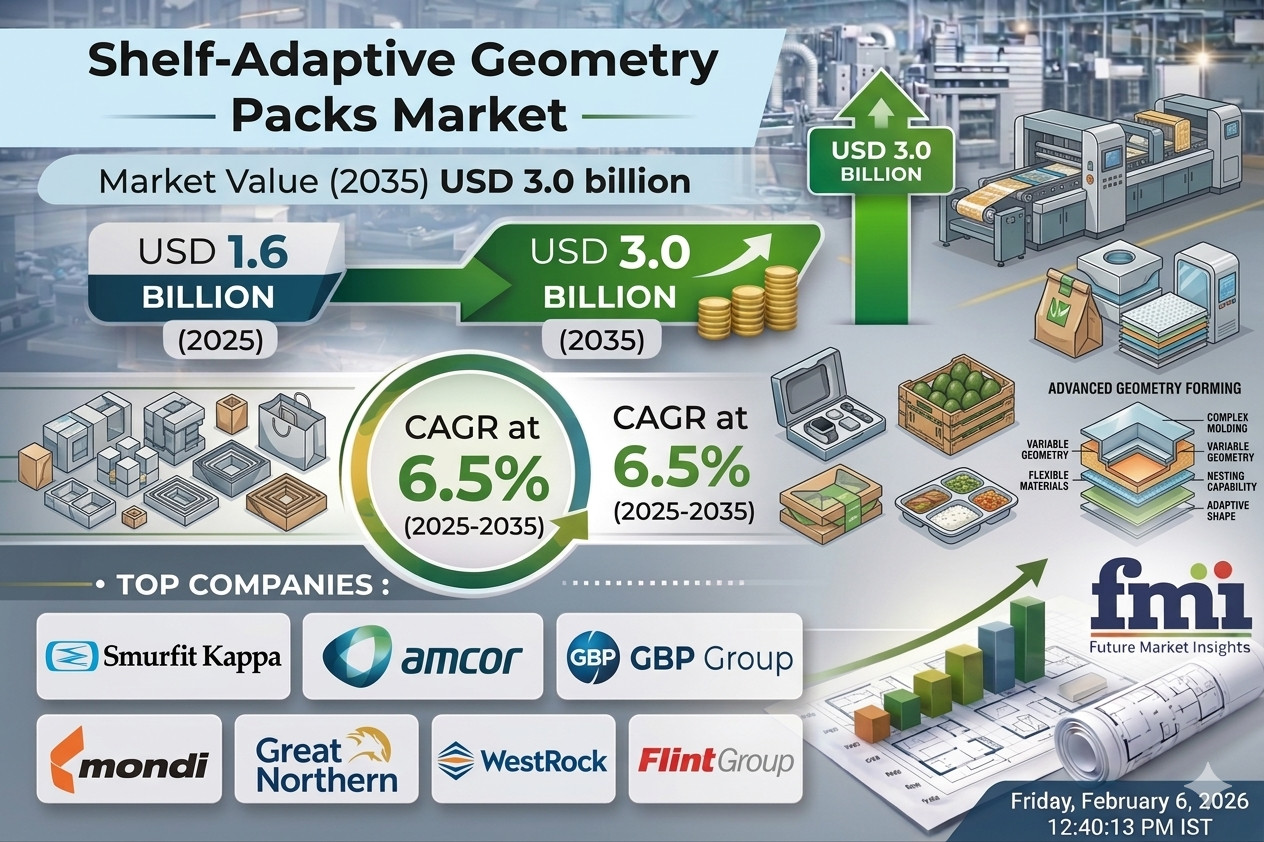

Shelf-Adaptive Geometry Packs Market Statistics Highlight USD 3.0 Billion by 2035

The shelf-adaptive geometry packs market is entering a decisive growth phase as retailers, brands, and logistics providers rethink how packaging interacts with increasingly dynamic retail environments. Valued at USD 1.6 billion in 2025, the market is projected to reach USD 3.0 billion by 2035, expanding at a CAGR of 6.5%. This growth reflects a structural shift toward packaging formats that can expand, collapse, or reconfigure in response to changing shelf layouts, automated replenishment systems, and space-constrained urban retail models. As e-commerce and physical retail converge, shelf-adaptive geometry packs are emerging as a bridge between logistics efficiency and in-store presentation. From modular retail displays to collapsible e-commerce packs, adaptive geometry is redefining how products move, store, and present across channels.

Industry Meaning

Shelf-adaptive geometry packs refer to packaging formats engineered to change shape, volume, or configuration without compromising structural integrity. These include expandable packs, collapsible cartons, shape-memory designs, and flexible modular systems. Their core purpose is to improve shelf utilization, transport density, and visual merchandising, while supporting sustainability goals. Unlike static packaging, these solutions respond to real-world retail variability—different shelf depths, automated stocking systems, and mixed-channel distribution. For brands, this means fewer SKUs for packaging, improved shelf consistency, and reduced material waste. For retailers, it translates into faster replenishment, cleaner displays, and more efficient use of space.

Request For Sample Report | Customize Report | Purchase Full Report - https://www.futuremarketinsigh....ts.com/reports/sampl

Strategic Outlook

The market’s strategic direction is shaped by three converging forces: retail automation, sustainability mandates, and customization at scale. Asia-Pacific leads adoption with a regional CAGR of 7.4%, driven by high-volume retail operations in China, rapid e-commerce growth in India, and design-led innovation in South Korea. Japan plays a distinctive role, focusing on premium, precision-engineered adaptive packs for cosmetics and luxury consumer goods. North America, led by the United States, is adopting adaptive geometry packs for personal care, household goods, and omnichannel retail, while Europe continues to push eco-efficient, recyclable shelf-ready designs supported by regulatory frameworks in Germany, the UK, and France.

Market Evolution

Between 2020 and 2024, demand accelerated as retailers and brands experimented with collapsible and shape-memory packs to reduce logistics costs and waste. These early deployments validated the operational benefits of adaptive formats, particularly in online-to-offline fulfillment models. From 2025 onward, the market is shifting from experimentation to standardization and scale. By 2035, adaptive geometry packs are expected to be embedded into mainstream retail and e-commerce packaging strategies, supported by advancements in recyclable laminates, automated folding systems, and digital design tools. The result is a market evolving steadily rather than cyclically, anchored in long-term efficiency gains.

Growth Opportunities

Several high-impact opportunities are shaping the next decade:

• Retail and e-commerce dominance – Accounting for 43.0% of demand in 2025, driven by automation and reusable pack formats

• Premium and cosmetic packaging – Especially in Japan and South Korea, where aesthetics and precision matter

• Emerging markets – India and Southeast Asia adopting lightweight, collapsible formats to modernize retail infrastructure

• Smart modular systems – Packs designed for quick assembly, disassembly, and reuse in urban logistics

• Sustainable materials innovation – Recyclable laminates and biodegradable films enabling compliance and differentiation

Emerging manufacturers are leveraging digital printing, 3D structural design, and adaptive folding mechanisms to compete alongside established players, particularly in short-run and customized retail formats.

Demand Patterns

Demand is segmented clearly by design, material, application, and end use:

• Expandable packs lead design types with 37.1% share, valued for adaptability and waste reduction

• Flexible laminates dominate materials at 38.4%, balancing strength, printability, and downgauging

• Retail display packaging accounts for 36.2%, driven by modular shelf layouts and visual merchandising

• Retail and e-commerce remain the largest end-use segment at 43.0%, reflecting omnichannel convergence

Regionally, South Korea leads growth at 7.4% CAGR, followed closely by Japan (7.3%), where adaptive packs are increasingly used in luxury and gift packaging. The US, Germany, the UK, China, and India all show growth in the 6.4–6.6% range, underlining the market’s global relevance.

Technology Trends

Technology is central to the evolution of shelf-adaptive geometry packs. Key trends include:

• Advanced recyclable laminates combining strength with environmental compliance

• Shape-memory materials that return to preset forms after compression

• Automation-ready designs compatible with robotic folding and shelf replenishment

• Digital printing integration for customization without added tooling costs

• Modular 3D pack engineering enabling rapid adaptation to different retail formats

These innovations are enabling brands to balance efficiency, aesthetics, and sustainability, while reducing total packaging SKUs and operational complexity.

Competitive Landscape

The market is moderately consolidated, with established global packaging leaders investing heavily in adaptive geometry innovation while emerging players focus on agility and customization.

Smurfit Kappa remains a key force, leveraging its design-to-market capabilities and expanding shelf-ready solutions across Europe and beyond. Amcor brings strength in flexible laminates and material science, supporting scalable adaptive formats for global brands.

Mondi continues to emphasize sustainable shelf-ready and modular packaging, while WestRock and DS Smith focus on recyclable, retail-efficient geometries aligned with circular economy goals. Regional and emerging players such as Packhelp are gaining visibility by offering customizable, digitally enabled adaptive packaging for direct-to-consumer brands.

Competition increasingly centers on design intelligence, material sustainability, and speed-to-market, rather than volume alone.

Executive-Level Insights

• Market Size (2025): USD 1.6 billion

• Forecast Value (2035): USD 3.0 billion

• Growth Rate: 6.5% CAGR

• Leading Design Type: Expandable packs (37.1%)

• Top Material: Flexible laminates (38.4%)

• Largest End Use: Retail & e-commerce (43.0%)

• Fastest-Growing Market: South Korea (7.4% CAGR)

• Strategic Drivers: Retail automation, sustainability, modular design

Conclusion

Shelf-adaptive geometry packs are moving from niche innovation to core retail infrastructure. As shelf layouts become more dynamic and sustainability more measurable, packaging that adapts rather than resists change will define competitive advantage. By 2035, brands and retailers that invest early in adaptive geometry will benefit from lower logistics costs, stronger shelf impact, and improved environmental performance, positioning this market as a quiet but critical pillar of next-generation retail packaging.

Why FMI: https://www.futuremarketinsights.com/why-fmi

Have a Look at Related Research Reports on the Packaging Domain:

Seam Tapes Market: https://www.futuremarketinsigh....ts.com/reports/seam-

Unidirectional Tape (UD) Market: https://www.futuremarketinsigh....ts.com/reports/unidi

Bamboo Straw Market: https://www.futuremarketinsigh....ts.com/reports/bambo

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.